TEPE Closes Year at 0.6 TEPE closed the year in the positives.

In December 2013, TEPE increased both year-on-year and month-on-month and closed the year in the positives. The 2013 average was at -1.2 points compared to the 2012 average at -3.8 points. Despite the average in the negatives, the year 2013 was better than 2012 for the retail sector. Concerning quarters, 2013 was the second best year for the sector after 2011.

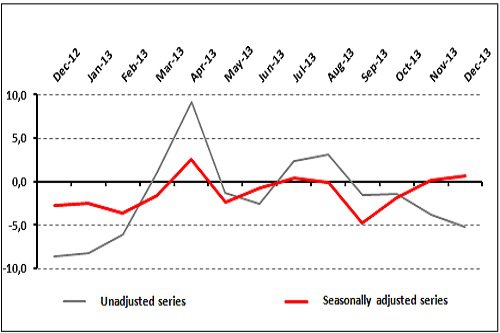

Expectation for sales in the next 3 months demonstrated a similar outlook with the average reaching 16.1 points in 2013 compared to 10.9 points in 2012. Upon quarterly figures, expectations for sales in the next 3 months had higher values in all four quarters in 2013 than in 2012.

The retail sector had a higher business volume in 2013 compared to 2012 as suggested by the anticipation for business recovery. The balance value of the volume of business activities had an average of -27.9 points and -22.1 points in 2012 and 2013, respectively. The sector performed better in 2013 compared to 2012 also on the basis of quarterly figures.

In December 2013, TEPE maintained the upwards trend started in October and had a value of 0.6. TEPE therefore increased by 0.5 points month-on-month and by 3.3 points year-on-year. The surge was driven by the level of business activities compared to the last 3 months and sales expectations in the next 3 months.

Seasonally adjusted TEPE values were higher in 2013 than in 2012 except February and September. The 2013 average was at -1.2 points compared to the 2012 average at -3.8 points. Despite the average in the negatives, the year 2013 was better than 2012 for the retail sector.

29.4 percent of TEPE survey participants declared that they expected an improvement in their business activities in the next 3 months while 27.5 percent expected deterioration. 43.1 percent of the participants declared that they did not expect their business activities to change. The balance value of the expectations for the next three months was 17.6 points in December 2013. Expectations therefore increased by 2.3 points year-on-year and decreased by 0.4 points month-on-month.

With seasonally adjusted series, expectations for the next 3 months were weaker in February, September, and October in 2013 compared to 2012. Expectation for sales in the next 3 months demonstrated a similar outlook with the average reaching 16.1 points in 2013 compared to 10.9 points in 2012.

Upon quarterly figures, expectations for sales in the next 3 months had higher values in all four quarters in 2013 than in 2012. According to this, it can be concluded that 2013 was a year of higher expectations for retailers compared to 2012.

22.3 percent of TEPE survey participants declared an improvement in their business activities compared to the year before while 37.8 percent declared deterioration. 39.9 percent of the participants declared that business activities did not change compared to 2012. The balance value of the volume of business activities in December 2013 compared to the same period in the previous year was minus 17.8 points. Anticipation for year-on-year recovery in business activities therefore decreased by 3.7 points compared to November 2013 and increased by 3.3 points compared to December 2012.

Seasonally adjusted series on the business volume suggests that 2013 values were higher than 2012 values except for September. The balance value of the volume of business activities had an average of -27.9 points and -22.1 points in 2012 and 2013, respectively.

The sector performed better in 2013 compared to 2012 also on the basis of quarterly figures. Based on this, it can be concluded that the retail sector had a larger business volume in 2013 than in 2012.

Compared to December 2012, electrical appliances, radio and televisions sector was the best performer, followed by the furniture, lighting equipments and household articles, “others” (gas station, pharmacy, perfumery, hardware, glassware, stationery etc), and motor vehicles sectors. The year-on-year increase in business activities was higher than the average in the named four sectors while it was lower than the average in the non-specialized stores sector. Textile, ready-made clothing, and footwear and food, beverages and tobacco products sector declined in December with the latter demonstrating the sharpest decline.

Question-based assessment of TEPE survey results suggests that compared to November 2013, expectations for orders, sales and employment in the next 3 months and for the number of stores in the next 12 months, as well as the level of business activities compared to the past 3 months and past year declined. Compared to December 2012, all expectations and conditions improved except for the expectations for orders, sales and employment in the next 3 months and for the number of stores in the next 12 months.

Konya’s retail sector performed better than 2012 in 2013

In the context of the Konya Province Retail Confidence Index (KOPE) carried out in cooperation by Konya Chamber of Commerce (KTO) and the Economic Policy Research Foundation of Turkey (TEPAV), face-to-face interviews with 300 retailers from Konya have been carried out on a monthly basis since February 2012.

In December, KOPE had a value of -1.4 compared to TEPE at -5.1. KOPE which had been decreasing since September moved up in December. The Index declined year-on-year by 8 points while TEPE increased by 3.4 points. Konya’s retail sector performed better than overall Turkey in December.

Expectations for the future as well as the level of business activities compared to the past increased in Konya’s retail sector.

- TEPAV Retail Confidence Indicator - TEPE